Introduction to Personal Income Tax Deductions

Emeka Okonkwo had just received his payslip for March 2026 and was staring at the numbers in disbelief. His colleague, Ngozi Adeyemi, leaned over from her desk at their Lagos marketing firm and asked, ‘Emeka, why do you look like you just saw a ghost?’ Emeka shook his head slowly. ‘I earn ₦4.5 million a year,’ he said, ‘but I have no idea how much tax I’m actually supposed to be paying.’ Ngozi smiled knowingly. She had recently attended a seminar on the new Nigeria Tax Act 2025 and had finally understood how her own deductions worked.

‘Sit down,’ she told him. ‘Let me explain everything from your rent to your pension.’ By the time Ngozi finished walking Emeka through the law, he realised he had been overpaying tax because he never declared his annual rent or his life insurance premium. Their HR manager, Chukwuemeka Duru, overheard the conversation and immediately called a staff-wide briefing. That afternoon, everyone from Adaeze the accountant to young Seun, who had just started his first job, learned exactly what the Nigeria Tax Act 2025 allows them to deduct from their taxable income, and how to do it correctly.

THINGS TO KNOW ABOUT PERSONAL INCOME TAX DEDUCTIONS

The Nigeria Tax Act (NTA) 2025, signed into law in June 2025 and effective from January 1, 2026, represents the most sweeping reform of the Nigerian tax system in decades. It formally repeals the long-standing Personal Income Tax Act (PITA) and consolidates several existing tax laws into one unified legislative framework. For millions of Nigerian employees and self-employed individuals, this change is not merely administrative, it directly affects how much of their hard-earned income they take home every month.

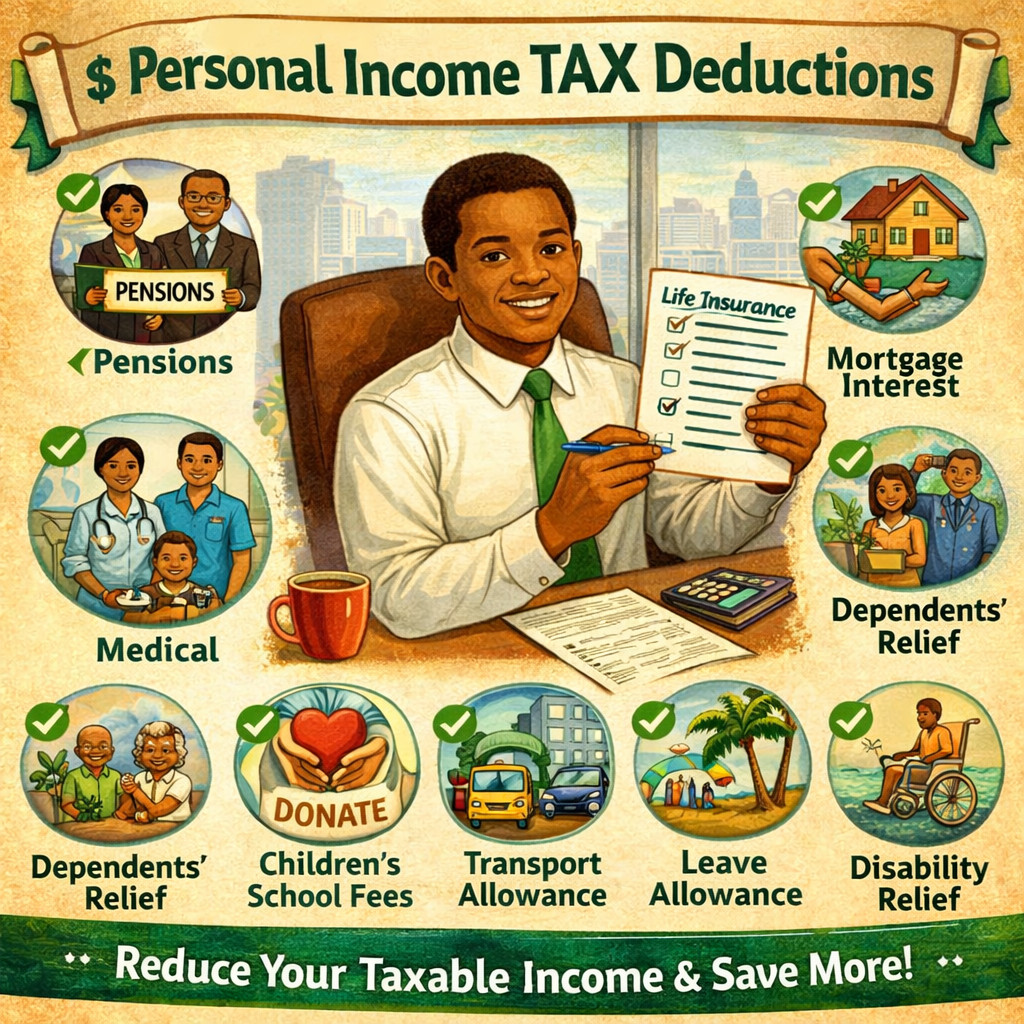

Central to the new law is a restructured system of personal income tax deductions. The familiar Consolidated Relief Allowance (CRA), which many taxpayers relied upon under the old PITA, has been abolished and replaced with more targeted, verifiable reliefs such as Rent Relief, Pension Contributions, and Life Insurance Premiums. The underlying philosophy of the NTA 2025 is clear: relieve low and middle-income earners of disproportionate tax burdens while requiring high-income earners to contribute more. This article explains the key deductions available under the Act, the specific sections of the law that will ensure every Nigerian remains tax compliant.

Personal Income Tax Deductions: Consolidated Relief Allowance

Under the old Personal Income Tax Act, the Consolidated Relief Allowance gave taxpayers a deduction of 20% of gross income plus a flat base amount, which many used as a blanket reduction without needing to prove any specific expenditure. The NTA 2025 completely abolishes this. Section 30(vi) of the Act formally removes the CRA and introduces in its place a set of specific, evidence-based deductions that taxpayers must actively claim and support with documentation.

The most prominent of these new deductions is the Rent Relief, introduced under Section 30(2)(a)(vi). This provision allows an individual to deduct 20% of the annual rent they pay, subject to a maximum cap of ₦500,000, whichever is lower. Crucially, the taxpayer must accurately declare the actual amount of rent paid meaning documentary evidence such as rent receipts or tenancy agreements will be essential during any tax audit. This is a direct response to Nigeria’s housing cost crisis, particularly in cities like Lagos and Abuja, where a significant portion of a worker’s salary goes toward accommodation.

Pension contributions remain deductible under Section 30(2)(a)(iii). Only the employee’s portion which stands at 8% of the employee’s basic salary, housing allowance, and transport allowance as required under the Pension Reform Act qualifies for deduction. The employer’s 10% contribution is excluded from the employee’s taxable income entirely, meaning it is already treated as a non-taxable benefit. Additionally, contributions to the National Housing Fund (NHF) are deductible under Section 30(2)(a)(i). Employees earning ₦3,000 or more per month are required to contribute 2.5% of their basic salary to the NHF, and this contribution is fully deductible. Similarly, contributions made under the National Health Insurance Scheme (NHIS) are deductible under Section 30(2)(a)(ii), provided the taxpayer can present proof of payment.

Life Insurance and Mortgage Interest

Beyond housing and pension, the NTA 2025 extends deductibility to life insurance premiums under Section 30(2)(a)(v). Any annuity or premium paid by a taxpayer in respect of insurance on their own life or that of their spouse or a deferred annuity contract is fully deductible. This provision encourages Nigerians to engage in long-term financial planning while simultaneously reducing their tax liability.

For homeowners, Section 30(2)(a)(iv) permits the deduction of interest paid on a loan taken to develop or purchase an owner-occupied residential house. The property must be occupied by the owner, and proof of interest payments must be presented to claim this relief. This provision is particularly important for middle-class Nigerians. The people paying off mortgages and have historically received little recognition in the tax code for doing so.

Personal Income Tax Deductions in relation to Zero-Tax Threshold

One of the most significant and immediate changes under the NTA 2025 is the expansion of the zero-tax threshold. Section 58 of the Act establishes that the first ₦800,000 of an individual’s annual income is taxed at 0%. This effectively creates a tax-free zone for the lowest-income bracket. Going further, Section 4(5) provides that individuals earning the national minimum wage or less are completely exempt from personal income tax. Once all eligible deductions are subtracted from gross income, the resulting figure known as Chargeable Income is taxed according to a new progressive rate structure:

- 0% on the first ₦800,000

- 15% on the next ₦2,200,000

- 18% on the next ₦9,000,000

- 21% on the next ₦13,000,000

- 23% on the next ₦25,000,000

- and 25% on income above ₦50,000,000.

For compliance purposes, Section 21(p) of the Act makes clear that any expense on which VAT was not charged, where applicable, or where relevant duties were not paid, will not qualify as a deductible. This places a firm documentation burden on taxpayers who wish to claim reliefs.

Conclusion

The Nigeria Tax Act 2025 marks a decisive shift in how the country approaches personal income taxation. By replacing the broad Consolidated Relief Allowance with specific, document-backed deductions including Rent Relief, Pension Contributions, NHIS, NHF, Life Insurance Premiums, and Mortgage Interest the law demands greater transparency and engagement from every Nigerian taxpayer. Low and middle-income earners stand to benefit the most, particularly those who actively declare qualifying expenses. High-income earners above ₦50 million face an effective marginal rate of 25%.

Like Emeka Okonkwo in our opening story, many Nigerians are currently leaving money on the table simply because they do not know what the law allows them to claim. Understanding these personal income tax deductions is no longer optional, it is a matter of financial literacy, legal compliance, and economic self-preservation. Whether you are a salaried employee, a professional, or self-employed, a thorough understanding of Sections 4, 21, 30, and 58 of the Nigeria Tax Act 2025 is essential to managing your tax obligations correctly and confidently.

Contributors

Lead Partner, EKO SOLICITORS AND ADVOCATES

Faith Ogunleye

Graduate Trainee, EKO SOLICITORS AND ADVOCATES

Idowu-Agida Nifemi

Counsel, EKO SOLICITORS AND ADVOCATES